The return of a high-frequency trading portfolio comes from a deep understanding of market microstructure. Every mispricing is fleeting; only extreme code performance and low-latency execution can consistently capture these opportunities.

AI technology makes signal mining, factor construction and risk management more systematic. From data cleaning and feature engineering to real-time decisions, models run through the whole research chain, keeping returns explainable and reviewable.

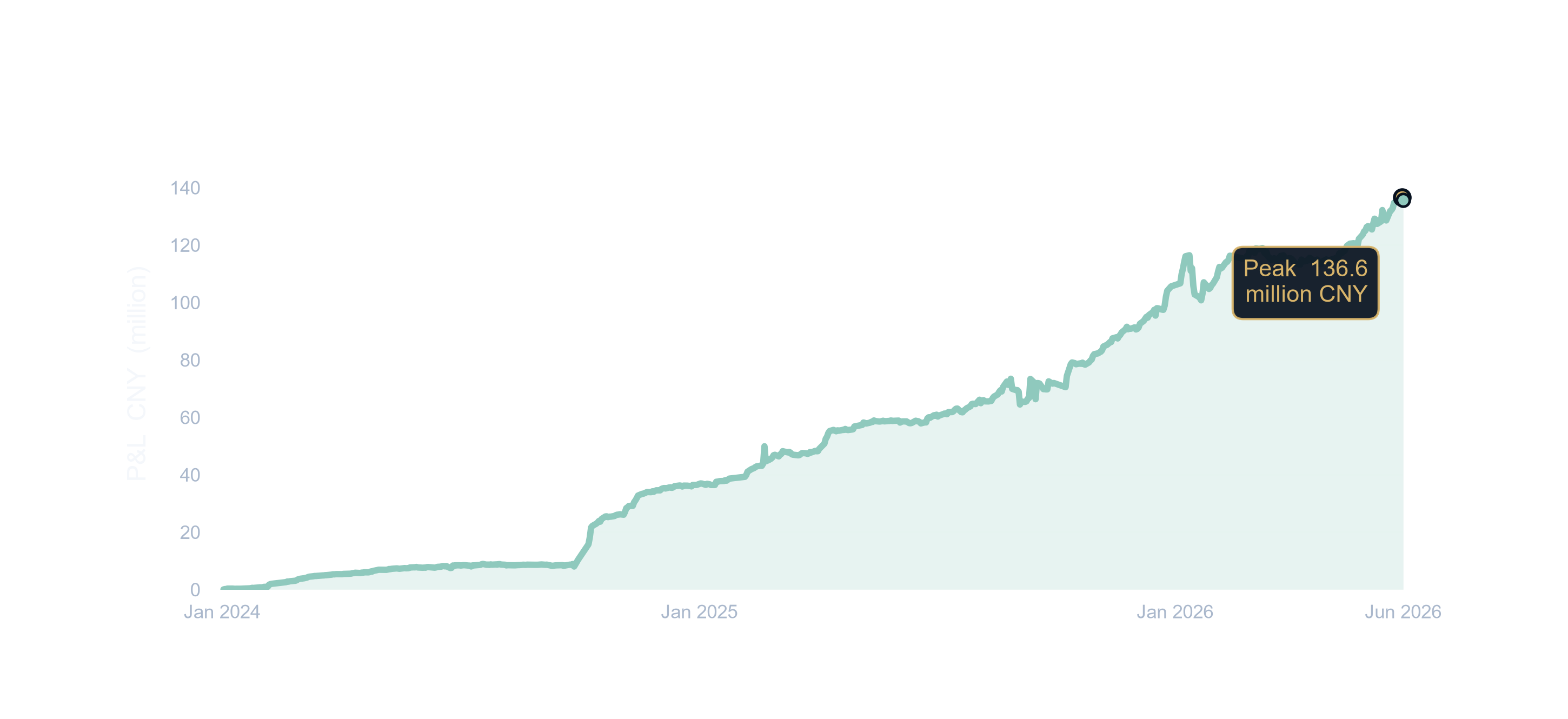

A high-Sharpe, low-drawdown profile rests on research discipline: rigorous out-of-sample validation, reasonable transaction-cost assumptions, executable risk boundaries, and continuous review of every strategy iteration.